Even the most conservational Filipino shopper can no longer deny the appeal of most buy now pay later apps. With incredible customer services and undeniable benefits, these apps are slowly claiming dominance on all shopping platforms (including digital purchases). It’s time we sat down to discuss what exactly they entail!

This insightful article has the answer you are looking for. We also dive further into some recommended options on the Philippines market, streamlining your e-commerce experience even more. Let’s get started!

Table of Contents

What Is Buy Now, Pay Later?

Buy Now Pay Later (BNPL) is a short-term type of financing, allowing consumers to buy items and make payments at future dates (often with no interest fees). To sum it up, consumers will hand in some upfront money for a particular purchase – before paying the remainder in predetermined installments.

Often regarded as “installment loans for sale points”, these BNPL services have been more common in recent years, particularly for online shoppers. Aside from the aforementioned interest-free plans, they also receive faster approval than credit lines and standard credit cards.

In most cases, BNPL has no impact on credit scores. Still, late payments (or, worse, failed payments) can lead to their irreversible damage.

How Do Buy Now Pay Later Apps Work?

Not all BNPL programs are the same. Each brand issues its respective conditions and terms. But overall, installment loans for sale points operate under these lines:

- Customers make purchases at specific retailers that participate in that BNPL program. They will select the “buy now pay later” option at the checkout.

- When you receive approval (you will know that in seconds), the next step is to make small down payments. (ex: 20% of the total purchase amount).

- After that, pay the remaining cash across several interest-free installments. You can do so via bank transfers or checks. Some programs automatically deduct payments from bank accounts, credit cards, or debit cards.

Keep in mind that not every purchase is eligible for BNPL financing. Also, there can be certain limitations on the number of products that can be financed this way.

Both BNPL and credit cards permit delayed payments, but they are not identical. When using credit cards, customers are only expected to make minimum payments due on their cards every month. Interest will accrue for your remaining amount until it’s paid off 100% (the only exception is when you use cards with no introductory APR).

On the other hand, BNPL programs never (or rarely) charge fees or interests. Instead, they have fixed repayment schedules – usually every few weeks or even months. The apps will inform you beforehand of the required amount for each time – which often stays unchanged in most cases. We can compare such payment plans to unsecured consumer or personal loans.

Want to get cash fast and easy?

Top 3 Buy Now Pay Later Apps in Philippines 2023

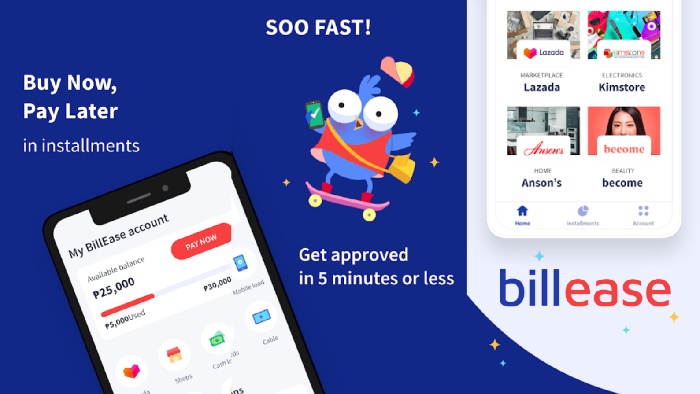

1. BillEase

Of course, it would be a crime to skip BillEase! It was released around 2017, from which the company only continues to grow.

With its current development team of 100 members, it’s easily one of the best buy now pay later services in the Philippines. Financial issues and other relevant dilemmas will be only a piece of cake thanks to its wonderful customer support!

To be more specific, BillEase makes the shopping experience easier for most Filipinos with consistent installment plans, allowing you to split your purchase into three to twelve months. All you need to do is to browse through items you wish to buy from partnered stores with BillEase – and then select BillEase payments. Long-time usage will give you access to further discounts, opportunities, and features!

2. Cashalo

Cashalo is a renowned mobile platform designed by Oriente and JG Summit, which brings millions of financial opportunities to its Filipino citizens! The brand provides both iOS and Android versions to ensure every customer from 18 onward can get their hands on fast loans.

Since some people still feel confused about its design, here are some basic steps of how Cashalo should work for you:

Step 1. Download the app to your mobile phone.

Step 2. Register into the app using your phone number (in the Philippines, of course)

Step 3. Provide identity verifications to officialize your account.

Step 4. Choose a loan amount, repayment schedule, and duration periods.

Step 5. The money you require will arrive in your bank account within 30 minutes. Use this loan to pay for whatever item you want to purchase.

Step 6. Remember to pay Cashalo back on the due date.

3. LazPayLater

Lazada has been known to partner with multiple fintech brands in the Philippines for Buy-now-pay-later services. Little do people know that the app also establishes its own BNPL system: the LazPayLater – or Lazada Loan though this program seems to be only available to a selective number of users at the moment.

With LazPayLater, customers can get maximum credit limits of ₱15,000, which they can spend on Lazada product purchases. Nevertheless, keep in mind that using these amounts of cash for digital goods (gift cards, e-vouchers, mobile loads), and jewelry is out of the question.

The best thing about Lazada BNPL lies in the free-of-charge policy. Yes, there’s no subscription fee, processing fee, handling fee, or any other charges often found in similar applications. And as long as you remember to pay your loan in 45 days, LazPayLater won’t even demand any interest rate. How wonderful!

Conclusion

This article has discussed all essential information regarding buy now pay later apps for Fillipinos. We have also introduced three promising options on the market with incredible rewards and well-praised customer service.

Hopefully, your shopping journey will reach new heights! For more questions, do not hesitate to reach out.

Want to get cash fast and easy?